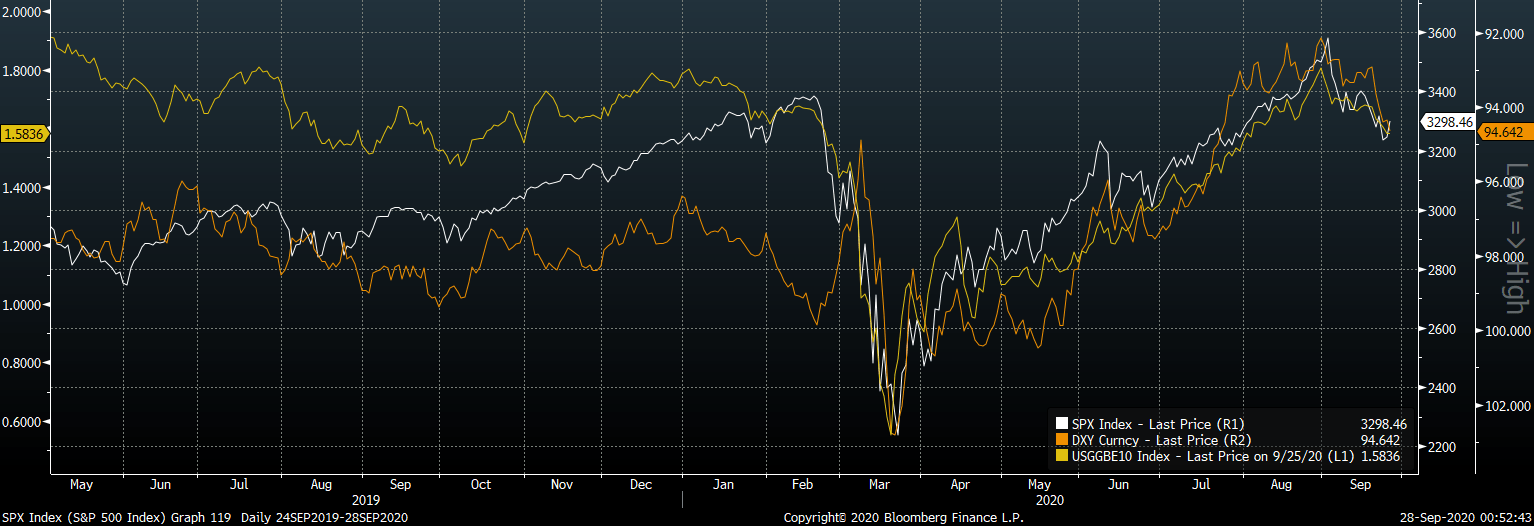

- The U.S. dollar has become highly correlated with U.S. stocks over recent months. The 100-day rolling correlation between the SPX and the DXY is currently the most negative on record.

- Recent U.S. equity weakness has put renewed upside pressure on the dollar, but we will likely need to see considerably more equity weakness for the dollar bull market to resume.

- Divergences between the DXY and the fair value implied by real yield spreads have previously provided a good indication of the performance of the DXY over the subsequent two years.

- The current spread is consistent with 4-5% annual DXY declines over the next two years. With this in mind, in order for the dollar to strengthen further, we would likely need to see significant U.S. equity weakness, sufficient to drag down inflation expectations enough to cause a spike in real yields.

After calling for dollar weakness at the height of the so-called dollar shortage back in March (see “Dollar Shortage A Red Herring“), we have seen the dollar index decline in lockstep with the rising equity market. While the recent U.S. equity correction has put renewed upside pressure on the dollar, we will likely need to see considerably more equity weakness in order for the dollar to resume its longer-term bull market. Given the ongoing decline in U.S. real yields relative to the eurozone, Japan, and the U.K., a U.S. equity market crash would be a necessary yet not sufficient condition for a resurgence in the U.S. dollar.

DXY-SPX Correlation At Record Levels

Movements in the dollar have become highly correlated with movements in U.S. stocks over recent months. The 100-day rolling correlation between the SPX and the DXY is currently the most negative it has ever been at -0.95.

DXY, SPX, and 100-Day Rolling Correlation

Source: Bloomberg

Both markets continue to be driven by broad risk appetite and the inflation/deflation trade. The chart below shows how the dollar’s decline and the equity rally has gone hand in hand with rising inflation expectations. This correlation looks set to remain in place in the near term. Any sharp equity market decline would likely occur alongside a drop in inflation expectations, placing upside pressure on U.S. real yields, and causing dollar strength.

DXY (inverted), SPX, and 10-Year Breakeven Inflation Expectations

Source: Bloomberg

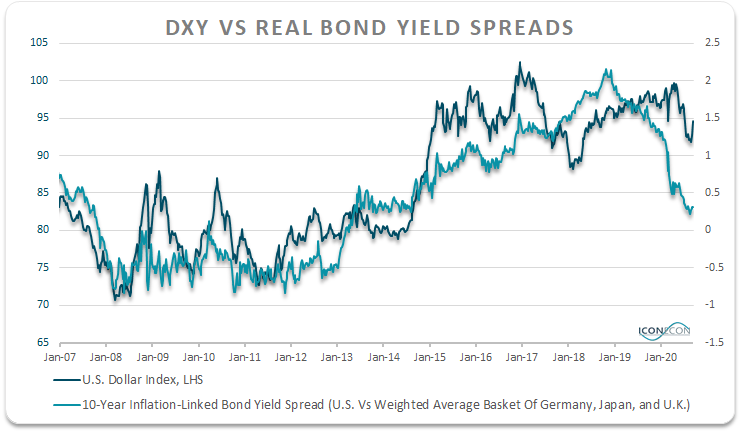

Real Yield Spreads Remain Dollar Negative

However, despite the recent slight rise in U.S. real yields, the broader trend remains dollar bearish. The following chart shows the U.S. dollar index against the spread of U.S. 10-year real yields versus a weighted average basket of German, Japanese, and U.K. real yields. While the DXY is near two-year lows, real yield spreads are back at 2014 levels.

Source: Bloomberg, Author’s calculations

Source: Bloomberg, Author’s calculations

Divergences between the DXY and the fair value implied by real yield spreads have previously provided a good indication of the performance of the DXY over the subsequent two years. The current spread is consistent with 4-5% annual DXY declines over the next two years.

Source: Bloomberg, Author’s calculations

Dollar Needs A Renewed Rise In Deflation Fears

Another way to view the disconnect between real yield spreads and the DXY is to say that it would take a ~100bp rise in U.S. real yields in order for real yield spreads to rise back to levels consistent with the current level of the DXY. With this in mind, in order for the dollar to strengthen, we would likely need to see significant U.S. equity weakness, sufficient to drag down inflation expectations enough to cause a spike in real yields. It is worth bearing in mind though that declining U.S. equities would likely put downside pressure on European, Japanese, and U.K. equities and inflation expectations. This suggests we would need to see significant U.S. equity underperformance in order for the dollar to continue its recent rally.

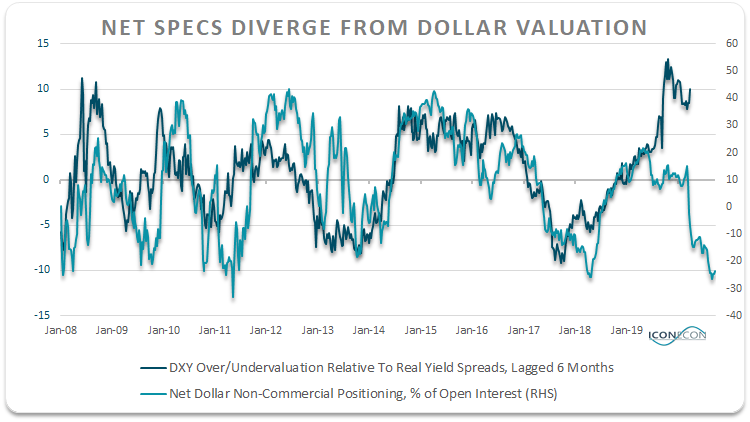

Bearish Dollar Positioning Is Not Necessarily Contrarian

Previous periods of dollar overvaluation relative to the fair value implied by real yield spreads have reflected bullish dollar sentiment. Rather than being a contrarian signal of an impending reversal, net non-speculative positioning has tended to act as a leading indicator.

Source: Bloomberg, Author’s calculations

Source: Bloomberg, Author’s calculations

As the chart above shows, swings in net non-commercial positioning as a share of open interest have tended to lead changes in the DXY relative to its fair value by around six months. Over the past six months, however, the dollar has significantly outperformed relative to real yield spreads despite a rise in bearish speculative positioning. We are not drawing any concrete conclusions from this other than to note that the high degree of bearish speculative positioning may not be the contrarian indicator that many dollar bulls expect it to be.