- Compared to the previous market peak back in February, U.S. stocks are more overvalued, market internals are even weaker, and the economic outlook is far worse.

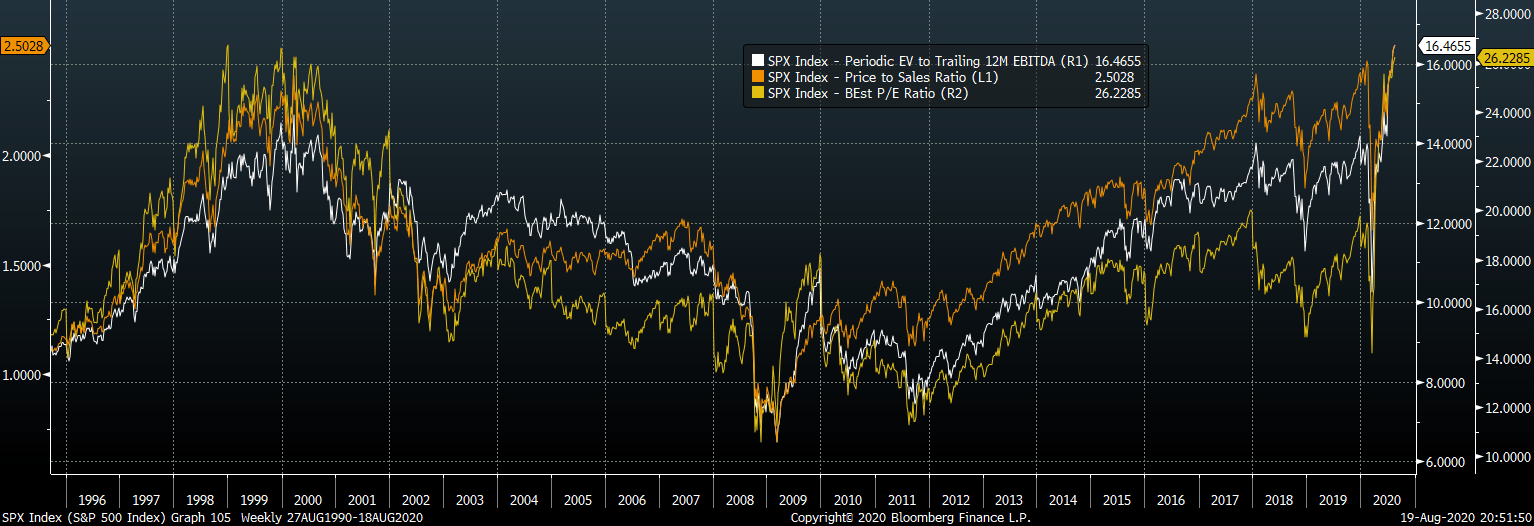

- The most historically reliable valuation metrics such as market capitalization to GDP, P/S, and EV/EBITDA, show the SPX is at its most overvalued on record.

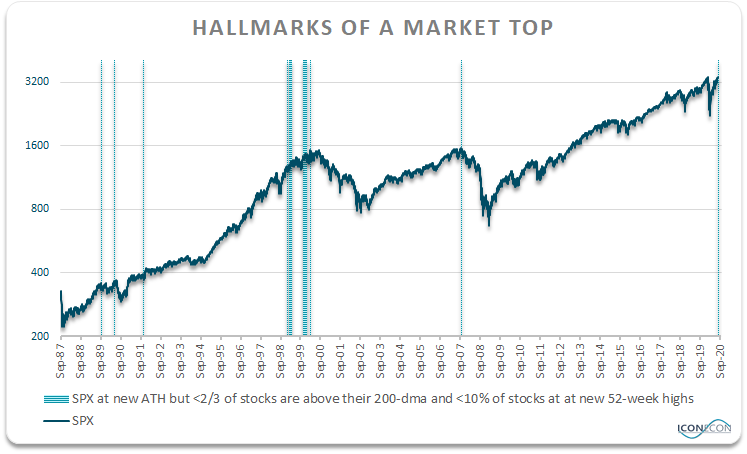

- Despite the SPX hitting new highs, only 6% of stocks posted new 52-week highs (versus 17% in February), while only 61% were trading above their 200-dma (versus 80% in February).

- The last time we saw the SPX hit a new all-time high despite similarly weak market breadth and participation was October 5, 2007, a few days before the market peak. The time before that was March 24, 2000, the very peak of the tech bubble.

- The fact that stocks have become cheaper relative to bonds is almost entirely irrelevant for the outlook for stocks themselves, and merely condemns balanced portfolios to their worst return prospects on record.

The SPX managed to close at a new all-time high yesterday as the market continues to defy deteriorating economic fundamentals, providing another great opportunity to enter short positions. Compared to the previous market peak back in February when we initially called for a crash (see here and here), U.S. stocks are more overvalued, market internals are even weaker, and the economic outlook is far worse. While we cannot rule out another leg higher, the risk-reward outlook is as negative as it has ever been.

The Most Overvalued Market Ever

Using valuation metrics that have been most closely correlated with subsequent returns in the past, the SPX is at its most overvalued on record. Such measures include market capitalization to GDP, price-to-sales, and EV-to-EBITDA, which strip out the impact of profit margins which tend to be highly cyclical in nature. Even the forward PE ratio, which assumes that profit margins remain at their highest levels on record outside the 2018-2019 period, is within a whisker of its 2000 all-time high.

SPX Valuations At New All-Time Highs

Source: Bloomberg

Of course, valuations have not at all deterred investors over recent months and years, or we would not be at the extreme levels we are today. However, this does not mean that they no longer matter as some analysts have concluded. We are open to the possibility that policy support for financial markets has meant that the old rules no longer apply and that valuations have moved to a higher equilibrium level. However, even if this is the case, which we highly doubt, all it means is that long-term returns will be far weaker than they have been in the past.

Market Internals Are The Weakest Since The 2000 Peak

Despite the SPX hitting a new closing high yesterday, only 6% of the index’s components managed to post new 52-week highs (versus 17% at the February peak), while only 61% of components were trading above their 200-dma (compared to 80% at the February peak). Furthermore, the number of declining issues has exceeded the number of advancing issues over the past five days. The last time we saw the SPX hit a new all-time high despite similarly weak market breadth and participation was October 5, 2007, a few days before the market peak which gave way to the global financial crisis. The time before that was March 24, 2000, the very peak of what would later be widely acknowledged as the largest speculative bubble in U.S. stock market history.

Source: Bloomberg, Author’s calculations

Source: Bloomberg, Author’s calculations

Economic Outlook Increasingly Stagflationary

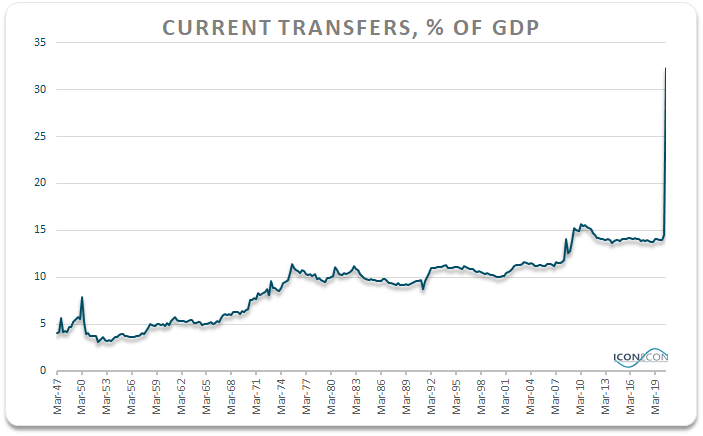

We argued back in March that stagflation was highly likely to result from the government’s increased involvement in the economy and our conviction on this is strengthening by the day (see ‘The Coming Stagflation And The Case For Silver‘). The incredible rise in government current transfer payments relative to GDP as a result of the COVID crisis, and the money printing that has been undertaken to pay for it will prove difficult to roll back, particularly as the electorate and politicians show no sign of appetite for fiscal austerity.

Source: Bloomberg, BEA

Source: Bloomberg, BEA

The ongoing deterioration in the social fabric of the U.S. as seen in the riots across many cities will not only undermine investment demand but will likely result in additional government spending and Federal Reserve money printing. History shows that in the case of sharply rising inflation, corporate earnings do not perform well even in nominal terms, while equity valuation measures tend to contract substantially.

A Weaker Outlook For Bonds Does Not Improve The Outlook For Stocks

The only factor that could be argued to have improved the outlook for stocks compared to the February peak has been the fact that the outlook for bonds has deteriorated even more, with the 10-year yield dropping almost 100bps since February. However, as we explained in ‘SP500: Low Bond Yields Do Not Justify High Equity Valuations’, the fact that stocks have become cheaper relative to bonds is almost entirely irrelevant for the outlook for stocks themselves.

Even if we ignore the fact that low bond yields in part reflect the weak outlook for real GDP growth, we should still not expect them to reduce the required equity risk premium. Investors have historically required high absolute returns on stocks regardless of bond yields because equities are risky assets, with downside volatility coming at the worst possible times such as when the economy heads into recession. Faced with declining dividend income and deteriorating employment prospects, investors tend to require a significant premium to own stocks relative to bonds, as we saw at the height of the March crash.

This Time Is Different, But Not In A Good Way

The fact that U.S. stocks are trading at record valuations in the face of a weak economy is seen as evidence that this time is different, and we certainly agree that it is. However, this is by no means a cause for cheer. The success that policymakers have had in propping up financial asset prices in the face of weakening fundamentals will come at the expense of future returns. As we argued in ‘Depression-Era Returns Await Balanced Portfolios‘, a balanced portfolio of 50% SPX and 50% 10-year bonds is now priced to achieve their weakest returns ever, including those seen during the Great Depression, with historical correlations suggesting -1.5% annual nominal total returns over the next 10 years. The only way investors on the whole are likely to achieve positive returns is if policymakers manage to produce enough inflation that nominal earnings rise enough to offset the likely decline in valuations. If this is the case, real returns would likely be far worse than we could even imagine.

Source: Bloomberg, Author’s calculations

Source: Bloomberg, Author’s calculations